The CSRD directive enables investors, financial analysts, and other stakeholders to evaluate companies' non-financial performance. It not only encourages these companies to develop more responsible business approaches but also radically transforms companies' scope of sustainability reporting.

The European Commission recently defined a common reporting framework for non-financial data through the CSRD. If your company isn't familiar with it yet, it’s time to dive in, and here at CtrlPrint we are happy to help you with this new reporting standard, thanks to our integrated CtrlPrint XBRL tagger, you can tag, review, and validate your report using the relevant taxonomies.

In this article, you will learn about the CSRD timeline and what it means for businesses in their sustainability practices.

Before we begin, if you are in need of a corporate reporting software for your CSRD submission, check how CtrlPrint can help you deliver compliant and captivating sustainable reports.

Key takeaways on the upcoming CSRD reporting

Here are our main takeaways regarding CSRD and how they might affect your company:

- CSRD requires companies to include their environmental and social impact in their Annual Report.

- Following the CSRD can boost a company’s reputation, attract investors, and help manage risks better.

- Companies need to be ready to start complying with these regulations as soon as January 2025, depending on their size and category.

Contents of this article:

What is CSRD and what does it do?

Why was CSRD introduced?

What are the benefits of CSRD?

What is the timeline of CSRD?

When will CSRD come into effect?

Final Thoughts

Frequently Asked Questions (FAQs)

What is CSRD and what does it do? Double Materiality Assessment (DMA) and Gap Analysis

The CSRD is an EU law that requires EU businesses, including some non-EU companies, to report their environmental and social impacts and how their ESG actions affect their business.

The goal of the CSRD is to provide clarity that helps investors, analysts, consumers, and other stakeholders to evaluate companies' sustainability performance and related business impacts and risks.

CSRD reporting is based on a double materiality assessment. This means that organisations must disclose information on how their business affects the environment, and also how their sustainability goals, measures, and risks impact their finances.

For example, in addition to reporting energy usage and costs, CSRD requires them to report emissions metrics, targets for reducing emissions, and information on how achieving those targets will affect their finances.

After finishing the Double Materiality Assessment (DMA), which is an important step in determining a company's reporting obligations under the CSRD, companies also need to conduct a Gap Analysis.

This analysis is important for identifying differences between an organisation's current data system and the standards mandated under the CSRD.

The Gap Analysis serves as a strategic method for pinpointing the disparities between a company's current ESG data collection and reporting, and the CSRD disclosure prerequisites. It acts as a guiding tool, steering companies through the unfamiliar terrain of sustainability reporting, enabling them to progress from their present status to achieving full compliance with CSRD.

All CSRD disclosures must be publicly available, and the CSRD mandates third-party auditing of all disclosures for accuracy and completeness. Also, let's not forget that under the CSRD the sustainability report must be part of the Annual Report.

Why was CSRD introduced?

In 2021, the European Parliamentary Research Service identified gaps in the Non-Financial Reporting Directive (NFRD), including inconsistent and costly data.

For this reason, CSRD was introduced to address these gaps and provide clearer, more comparable ESG disclosures, that help investors and analysts make better decisions.

What are the benefits of CSRD?

Complying with the CSRD presents several advantages for businesses. Let's see now 5 main reasons why your company should comply with CSRD and benefit from it.

- Better reputation

Following CSRD shows that companies care about sustainability and accountability for environmental, social, and governance (ESG) factors. This can improve a company’s reputation with customers, investors, and the community.

- Increased investor confidence

By offering clear, detailed insights into a company’s sustainability measures, the directive makes things more transparent and trustworthy for investors. This can lead to increased investment and higher market valuations.

- Competitive differentiation

Companies that follow CSRD can position themselves as leaders in sustainable practices, setting themselves apart from competitors.

- Improved risk management

The CSRD pushes companies to look at their ESG risks. This process makes organisations look closely at their operations for potential environmental and social risks, allowing them to develop effective strategies to fix them.

- Innovation and efficiency

Preparing for CSRD compliance often leads companies to evaluate their operations critically. Companies might find ways to use their resources better or cut down on waste. This can lead to smoother, more efficient operations.

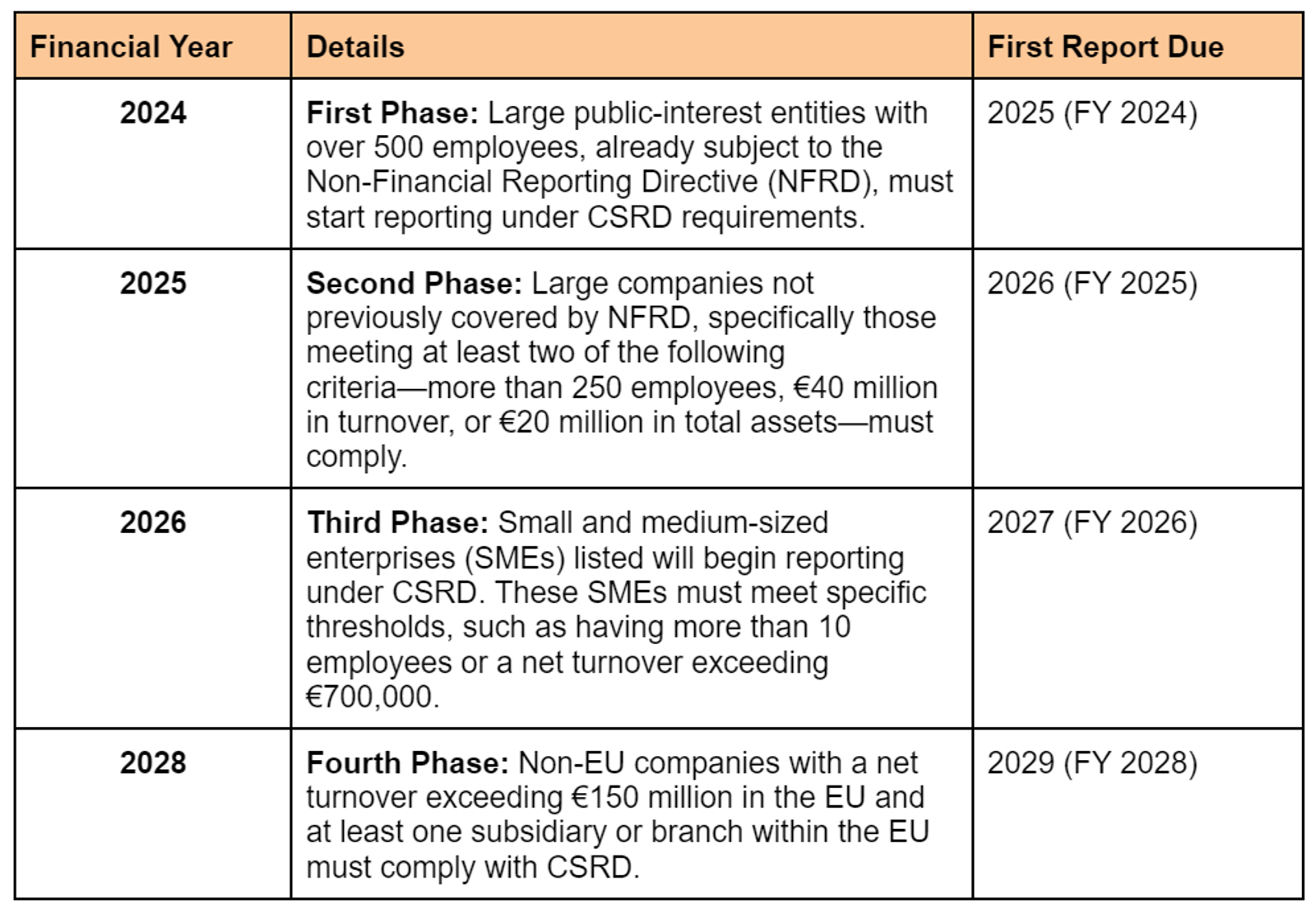

What is the scope and timeline of CSRD?

The Corporate Sustainability Reporting Directive (CSRD) sets specific timelines for companies to comply with sustainability reporting requirements based on size and classification.

CSRD was officially implemented on January 5, 2023, after receiving approval from the European Union Council. Here's a detailed overview of its implementation timeline:

Learn more about the timeline of the CSRD and policy-making timeline on the official European Commission website.

When will CSRD come into effect?

Individual EU countries will be responsible for enforcing CSRD compliance. Their regulators will monitor companies through audits and investigations.

As each country sets its own rules, enforcement, and penalties may vary.

Member states must adopt CSRD into their laws by July 6th, 2024, and penalties should be “effective, proportionate, and dissuasive.”

Final thoughts on CSRD

The Corporate Sustainability Reporting Directive (CSRD) is a crucial turning point for companies aiming to demonstrate their commitment to sustainability.

By acting now—collecting data and refining your processes—you can stay ahead of compliance requirements while driving innovation.

Are you looking for the right corporate reporting software to comply with the CSRD standards? Our experts at CtrlPrint are ready to help, contact us today to explore how our solutions can make a real difference to your sustainability reporting.

Frequently Asked Questions about CSRD (FAQs)

What is CSRD and ESRS?

The CSRD sets the stage for who needs to report and why, whereas the ESRS provides detailed guidelines on how to effectively carry out that reporting.

Is CSRD mandatory?

Yes, CSRD is mandatory for a wide range of companies operating within the European Union.

How many companies are in the scope of CSRD?

Nearly 50,000 companies are estimated to fall within the scope of CSRD.

Who is affected by CSRD?

The CSRD affects large EU companies and non-European companies listed on EU markets that meet two of the following criteria: over 250 employees, a balance sheet above €20 million, or revenue exceeding €40 million. It also applies to listed small and medium enterprises (excluding micro-enterprises), small credit institutions, captive insurance companies, and non-European groups with significant EU activities (over €150 million in turnover) and a large branch or subsidiary within the EU.

What happens if you are not complying with CSRD?

If a company fails to meet CSRD requirements, it could face serious consequences. Each EU member state will set penalties when they adopt the directive into their national laws. These might include financial fines or legal issues. Beyond that, non-compliance can hurt a company’s reputation, leading to lost trust from investors and stakeholders.

What are the penalties for CSRD?

Each EU member state is responsible for setting penalties under the CSRD. While the directive doesn't specify fines, countries can enforce monetary penalties, bar companies from public contracts, or even impose criminal charges in extreme cases. France, for example, fines up to €18,750 for not publishing a sustainability report, and companies may be excluded from government contracts. Severe offenses, such as obstructing audits, can lead to fines of up to €375,000 and up to five years of imprisonment.

How to start with CSRD?

To start with CSRD, first understand your company's scope and timeline. Assess your current sustainability practices and data collection. Develop a comprehensive sustainability strategy aligned with CSRD requirements. Invest in data management and reporting tools. Engage stakeholders and build internal capacity. Stay updated on CSRD developments and seek expert guidance.